10 Business Studies 3

Section outline

-

Tēnā koutou katoa!

Welcome everyone to Business Studies 2023.

I look forward to getting to know each of you and exploring the business world together. If you have any queries or concerns you are welcome to come and see me in M12 (upstairs in mountains) or by email akeung@mhjc.school.nz at any time.

I have setup a google classroom for our course and resources, notes and tasks will be updated for each lesson. If you are absent work will have been posted on the classroom page so it will be important for you to check in regularly.

The business studies course is guided by the following achievement objectives from the NZ curricuum:

Achievement Objectives:

Students will gain knowledge, skills, and experience to:

Level 2

- Understand that people have social, cultural, and economic roles, rights, and responsibilities.

- Understand how people make choices to meet their needs and wants.

- Understand how people make significant contributions to New Zealand’s society.

Level 3

Understand how people make decisions about access to and use of resources.

Level 4

- Understand how the ways in which leadership of groups is acquired and exercised have consequences for communities and societies.

- Understand how exploration and innovation create opportunities and challenges for people, places, and environments.

- Understand how producers and consumers exercise their rights and meet their responsibilities.

- Understand how formal and informal groups make decisions that impact on communities.

- Understand how people participate individually and collectively in response to community challenges.

-

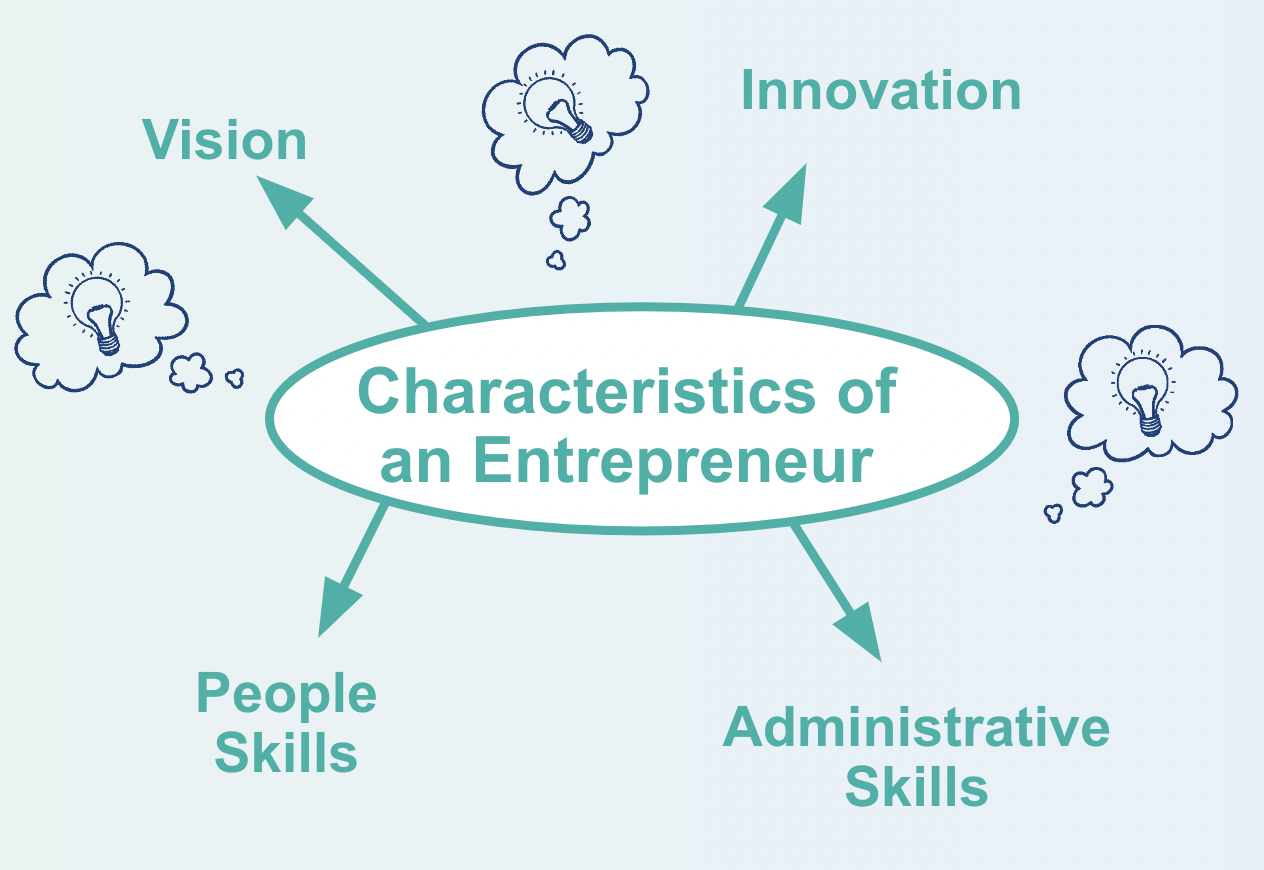

Enterprise, entrepreneurship, entrepreneurs

Learning outcomes:

Students will be able to:

- Describe the terms enterprise and entrepreneurship

- Recognise the qualities of successful entrepreneurs

- Describe innovation and recognise its importance in a successful business

In this module you will be learning about some entrepreneurs who are big thinkers. These people are all enterprising – that is they are bold and use their initiative to undertake new projects. Not only do they seize opportunities whatever the situation, they create opportunities for people to achieve more than might at first be thought possible.

Entrepreneurs are enterprising people who take risks, usually financial risks, to be able to put their big thinking into action. To fulfil our potential in this world, we all need to be enterprising. Some of us will also be entrepreneurs and create new businesses and social enterprises.

To think big you need to think without limitation, and put your fears to one side. Enjoy the journey!

-

Enterprising People

A person with an enterprising attitude says, “Find out what you can before action is taken.” Do your homework. Do the research. Be prepared. Be resourceful. Do all you can in preparation of what’s to come...

Enterprise is two things. The first is creativity. You need creativity to see what’s out there and to shape it to your advantage. You need creativity to look at the world a little differently. You need creativity to take a different approach, to be different.

What goes hand-in-hand with the creativity of enterprise is the second requirement: the courage to be creative. You need courage to see things differently, courage to go against the crowd, courage to take a different approach, courage to stand alone if you have to, courage to choose activity over inactivity.

And lastly, being enterprising doesn’t just relate to the ability to make money. Being enterprising also means feeling good enough about yourself, having enough self-worth to want to seek advantages and opportunities that will make a difference in your future. And by doing so you will increase your confidence, your courage, your creativity and your self-worth – your enterprising nature.”

-

Enterprising People Case Studies

Over the next week or so we will look at some enterprising people and identify the enterprising qualities that helped them to be successful.

Thomas Edison

“Our greatest weakness lies in giving up. The most certain way to succeed is always to try just one more time.” —Thomas Edison

Thomas Edison is one of the most famous and prolific inventors of all time. He exerted a tremendous influence on modern life, contributing inventions such as the incandescent light bulb, the phonograph, and the motion picture camera, as well as improving the telegraph and telephone. In his 84 years, he acquired an astounding 1,093 patents. Aside from being an inventor, Edison also managed to become a successful manufacturer and businessman, marketing his inventions to the public. However, it is also well known that Thomas Edison failed over 10,000 times when attempting to invent a commercially-viable electric lightbulb. Edison was a master of trial and error. He was not afraid to make hundreds, or even thousands, of mistakes before figuring something out.

What can we learn from Thomas Edison that can help us to be successful in our own personal endeavours?

-

Henry Ford

“Whether you think you can, or you think you can't – you're right,”

“Failure is only the opportunity more intelligently to begin again.”

The success story of Henry Ford is known as the father of the automobile and creator of the assembly line. While working as an engineer for the Edison Illuminating Company in Detroit, Henry Ford (1863-1947) built his first gasoline-powered horseless carriage, the Quadricycle, in the shed behind his home. In 1903, he established the Ford Motor Company, and five years later the company rolled out the first Model T. He helped bring transportation to the masses in America with his Ford Model T car. However, prior to this success both his first company and then his second company went bankrupt -

What is an entrepreneur?

The word ‘entrepreneur’ first appeared in the English language in the 1700s. It comes from the French verb ‘entreprendre’ which means to ‘undertake’ or to ‘do something’.

An entrepreneur is a person who sets up a business and takes risks in the hope of making money. They see a financial opportunity and act on it.

HOWARD WRIGHT WAS A NZ MOTOR MECHANIC WHO LOVED TO MAKE THINGS AND SOLVE PROBLEMS.

In the 1950s Howard started his own engineering business in a small workshop underneath his house in New Plymouth, New Zealand. He mostly made things out of wrought iron, like balustrades for stairs,

until he was approached by a nurse from the local hospital. Could he make a modern hospital bed like the ones they had seen in photos from overseas? Howard looked at the photos and talked to the nurse and decided he could. It wasn’t long before he realised he could in fact do a lot better, using the latest hydraulics. Howard’s fame and his hospital Beds spread around New Zealand and in the early 1960s he took the plunge and opened his first dedicated hospital bed factory.

Tasks on google classroom

-

Characteristics of Entrepreneurs

We will start looking at the characteristics of successful entrepreneurs

-

Learning outcomes:

- identify entrepreneurs that were innovative

- identify and describe the characteristics of innovation

- recognise the importance of innovation to business success & sustainability

Characteristics of Innovation

Innovation may have some of the following characteristics.

- Something “New” It is different to current models.

- Better than what exists: It new but also improved.

- Solves problems. Makes life easier or more convenient for users

- Has economic value: People would be willing to buy it

-

History of Innovation Task

You may do this task in pairs.

- Choose any invention or product.

- Make a slideshow to show any innovations to that product that have been developed over time. Show at least 3 innovations over time.

- Come up with what’s next? Create a slide to suggest new innovations that could be made to this product in the future and explain how it is innovative and has economic value.

-

-

Learning Intentions

- Investigate ways in which businesses distribute their products to customers.

- Explore examples of different distribution channels and what affects business's choice of channel.

- Can describe several ways to distribute products and the factors that affect this choice.

- Can provide examples of different distribution channels.

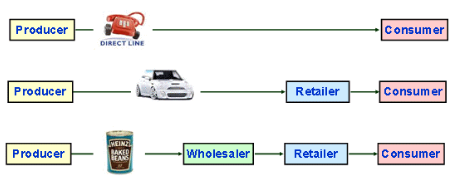

Place

Distribution (Place) ensures products are available to customers in the right quantity at the right time in the right place. It involves questions like:

- Where do consumers prefer to buy the product?

- How can we ensure the product is available to existing and potential customers?

- How important are speed, timing, cost, availability

- How much stock should we hold? Too little and we run out; too much and we tie up cash (that then cannot be used to pay daily expenses)

It depends on:- The product - is it perishable, technically complex, a convenience item?

- The market - is it geographically spread out, highly competitive?

- The business - is It large, supplying producers or consumers?

A distribution channel is the means by which the product moves from production to consumption. It might include:

A distribution channel is the means by which the product moves from production to consumption. It might include:- Retailer sells direct to households / end users / consumers

- Wholesaler sells products from different manufacturers to retailers; they 'break bulk' by putting large quantities into smaller packages

- Distributor have a contract to sell a manufacturer's products

- Agent a 'go-between' who never owns the product and earns commission eg real estate, insurance, travel.

- Franchisee allowed to trade under the the manufacturer's name; pays a fee and gives a share of the revenue to the franchisor

- Direct selling door to door, mail order, sales reps

Trends in distribution are:

- more out of town stores and malls (in Europe, malls are closing);

- fewer independent and more multiple / chain retailers;

- more franchises (eg Jim's mowing);

- online shopping and home delivery.

- drone and driverless delivery??

Extension activities (Optional)

Research the service that Uber Eats provides.

Research the service that Uber Eats provides.

Consider the impact on distribution of restaurant food.

How do restaurants and householders benefit?

Watch this video clip on drone delivery and discuss the impact on distribution channels and on different organisations that might be affected.

Watch this video clip on 3D printing and and discuss the impact on distribution channels and on different organisations that might be affected.

-

-

-

Learning Intentions

- Investigate ways in which businesses can price their products

- Explore examples of different pricing strategies and reasons for using each strategy.

- Explore the specific effect of changes in price on quantity sold and thus on profit.

- Can describe several key strategies for pricing products

- Can predict the effect of a price change on sales and thus profits.

Price

The price of o product sends strong messages to consumers. Would you buy a parachute in a sale at half price, or a perfume, for a valued friend, that was advertised as being low price, or petrol at a much higher price than competitors' prices?

Pricing strategies

- Cost-plus pricing - adding a percentage markup to the estimated unit cost.

- Penetration pricing - initial low price to encourage customers to try the product (but could send the message of low quality).

- Skimming - high price until competition forces it down

- Competitive pricing - in line with, or a certain percentage above, competitors' prices.

- Psychological pricing - appears closer to customer's perceived value (eg $3.99)

- Prestige price - to promote a luxury image (eg perfume)

- Price discrimination - price for the same product varies for different customer groups (eg students, off-peak travel).

- Loss leader - very low price attracts customers into the shop to buy other products at 'normal' prices.

- Promotional pricing - low price for a short time to renew customer interest or clear unwanted stock.

- Range pricing - prices of similar types of product kept within limits.

In your group, discuss which price strategy is being used in each of the examples below:

- A watch that’s very similar to others sold in the shops

- A toy sold for $1.95

- A tour operator sells holidays during the school holidays as well as at other times.

- A new brand of washing powder is launched - there are several similar ones already available

- A supermarket wants to cover the cost of vegetables and make a 100% profit as well.

- A new mobile phone has been developed that has extra features compared to the competition

Pricing Strategies

Cost-Plus Pricing

The business takes into account the cost of manufacturing the product and then adds on a profit mark-up. This can either simply cover costs or include an element of profit. It focuses on the product itself and does not take into account consumers’ expectations or perceptions. It is very easy to apply but the business may lose sales if their price is more than competitors.

Penetration Pricing

This is where the business sets the price lower than the competition to ‘penetrate the market.’ This is often useful when launching into a new or highly competitive market. It is typically used with mass market products – chocolate bars, food stuffs, household goods, etc. It is also suitable for products with long anticipated product life cycles.

Other benefits:

- Market share is quickly won.

- Encourages consumers to develop a habit of buying

- ‘Low’ price to secure high volumes

Price Skimming Strategy

This is where the business sets an initial high price for a unique product encouraging those who want to be ‘first to buy’ to pay a premium price. Later in the products life cycle they may then lower the price. It is usually used alongside a promotional campaign to create high demand for the new product before it is even launched. This strategy helps a business to gain maximum revenue before a competitor's product reaches the market. This is often used with technology products like mobile phones and devices.

Loss Leaders

This is where chosen goods/services are deliberately sold below cost to encourage sales elsewhere in the business. The business hopes that the purchases of other items more than covers ‘loss’ on item sold. It is typically used in supermarkets, e.g. at Christmas, selling bottles of coke at $0.99 in the hope that people will be attracted to the store and buy other products as well that will cover the loss made on the coke. Cell phones & contracts are another example.

Psychological Pricing.

This when particular attention is paid to the effect that the price of a product will have upon the consumers perceptions of the product. It may involve charging a very high price for a high quality product so that high income customers may wish to purchase it as a status symbol. E.g. Ferrari. Alternatively, it may charge a more reasonable or lower price so that consumers perceive it as an ‘affordable’, ‘value for money’ product.

Another example of psychological pricing is selling products for $199 instead of $200 is also an example of psychological pricing as it creates the impression of being much cheaper.

Another example of psychological pricing is selling products for $199 instead of $200 is also an example of psychological pricing as it creates the impression of being much cheaper.Promotional Pricing

This is when products might be sold “on sale” or at a lower price for a short period of time. It includes “buy 1 and get 1 free” deals. It is useful for getting rid of unwanted stock. It could help renew interest in a business if sales are falling. The challenge for businesses is that the lower price also reduces sales revenue and profits.

-

-

-

Learning Intentions

- Investigate ways in which businesses can price their products

- Explore examples of different pricing strategies and reasons for using each strategy.

- Explore the specific effect of changes in price on quantity sold and thus on profit.

- Can describe several key strategies for pricing products

- Can predict the effect of a price change on sales and thus profits.

Price

The price of o product sends strong messages to consumers. Would you buy a parachute in a sale at half price, or a perfume, for a valued friend, that was advertised as being low price, or petrol at a much higher price than competitors' prices?

Pricing strategies

- Cost-plus pricing - adding a percentage markup to the estimated unit cost.

- Penetration pricing - initial low price to encourage customers to try the product (but could send the message of low quality).

- Skimming - high price until competition forces it down

- Competitive pricing - in line with, or a certain percentage above, competitors' prices.

- Psychological pricing - appears closer to customer's perceived value (eg $3.99)

- Prestige price - to promote a luxury image (eg perfume)

- Price discrimination - price for the same product varies for different customer groups (eg students, off-peak travel).

- Loss leader - very low price attracts customers into the shop to buy other products at 'normal' prices.

- Promotional pricing - low price for a short time to renew customer interest or clear unwanted stock.

- Range pricing - prices of similar types of product kept within limits.

In your group, discuss which price strategy is being used in each of the examples below:

- A watch that’s very similar to others sold in the shops

- A toy sold for $1.95

- A tour operator sells holidays during the school holidays as well as at other times.

- A new brand of washing powder is launched - there are several similar ones already available

- A supermarket wants to cover the cost of vegetables and make a 100% profit as well.

- A new mobile phone has been developed that has extra features compared to the competition

-

-

Assessment 2 information

Assessment 2 is to be confirmed, but will be based on your work towards Market Day.

You'll produce a group Business Plan for your Market Day business. The deadline for submitting the Plan is Term 3 Week 9. More info to come.Market Day

Market Day is Term 3 Week 10 Thursday (21st September) from 1:15pm to 1:50pm. Food items are allowed.

Lost

We've started by identifying that there's a challenge that we're facing - to design, make, market and sell a product.

Rules:

- No on-selling existing products (eg Sprite) - make products from raw materials.

- Year 10s must have original, creative and high quality ideas & products.

- A product is

- a good (food, artwork, craft, food, soap, plants, etc) or

- a service (wash, paint, advertise, organise, etc) - No cooking at school and No meat. No entering the Food Tech room.

- Maximum of 3 group members

- Business Plan MUST include Health & Safety procedures, especially with food (photo evidence they were followed is needed).

- Promotion & Advertising on TV / poster permission from Whanau Dean or DP.

(Any Social Media ads are proofread by the Business teacher) - On Market Day, remove all signs; don't leave 'bike shed' until teacher OKs it.

- Think enviro friendly. Use correct bins for your packaging, etc.

Resources

Simon Sinek's Golden Circle idea will help you be successful

https://www.ted.com/talks/simon_sinek_how_great_leaders_inspire_action?language=en

Here's a Business Plan template that might help

https://www.business.govt.nz/getting-started/business-planning-tools-and-tips/how-to-write-a-business-plan/

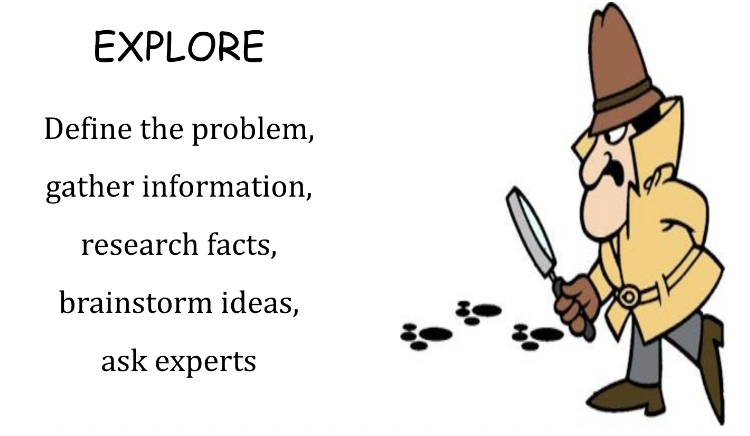

(Link to Botany South stats)Learning Process for 'Market Day'Explore

In your small group, brainstorm 100 words relating to ideas for products. Do NOT discuss the words. In particular, do NOT ridicule anyone for strange, left-field ideas, as it's these ideas that can lead to original, innovative products that other teams have not thought of.

Here are some links to help you get started:

Wood stick friends

Rock friends

Models from drinks cans

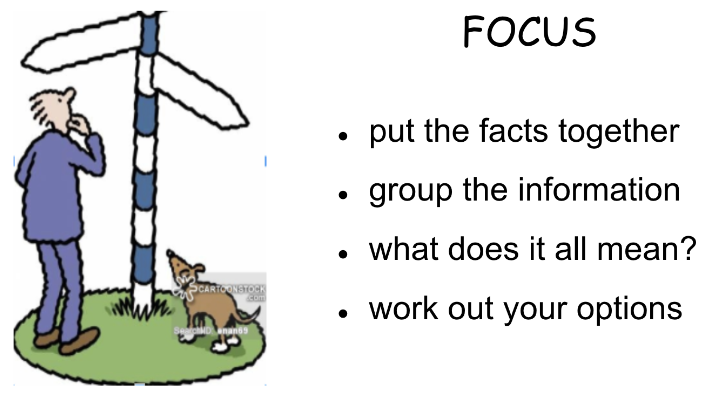

Bottle top jewelleryFocus

Group your brainstormed words into 2 or 3 general areas (eg brownies, cakes and muffins could be grouped under sweet baking).

When you have 2 or 3 broad possible areas, do research online and think of skills and knowledge that you can access (team members or their family and friends) that might lend themselves to one of the ideas.

Choose one product / area to focus on.

Here's a link to your brainstorms -

The 6 sections of the Business Plan are:

Introduction

(business description - briefly the team, product, aim or purpose, specific SMART goals, timeline)Market research

(methods, findings, SWOT analysisMarketing

(marketing mix - Price, Product (incl packaging), Place, Promotion)People

(organisation chart of members & roles, responsibilities)Finance

(budgets & graphs explained, sources of finance, sales forecasts, costs & revenue)Operations

(running the business (eg production, cash, quality control, health & safety, equipment)Log book

(diary of meetings, issues, etc) -

Use a Business Plan template and resources to record the who, what, when, how, why of your business idea.

Starting a business

Resources

- Xero process:

https://www.xero.com/nz/resources/small-business-guides/how-to- Shopify - starting a business:

https://www.shopify.co.nz/guides/new-zealand/business-structures -

SUBMIT Business Plan!

-

New deadline for assignment

Term 4 Week 2

Monday 16th October

5pm -

Learning Intentions (based on NZ Curriculum Level 5 Achievement Objectives)

- Understand how economic decisions impact on people, communities, and nations.

Understand how people’s management of resources impacts on environmental and social sustainability

- Able to explain the definition of economics (scarcity, resources, wants, etc.

- Can share examples of how economics affects our everyday lives

Economics

Economics affects everything you, your friends and family do. It is the study of how to allocate scarce resources in order to satisfy unlimited wants and needs. Put simply, it's deciding what OUTPUTS (products) to produce and what INPUTS (resources) to use to produce them.

For example, should we: only use public transport, build more dams to encourage dairy farming in drought-prone regions, use nuclear powered ships, employ more nurses, pay politicians higher salaries, pay university fees out of taxes, have a larger army, charge tourists more to walk the Milford Track, allow only 2 companies to control all supermarkets, limit the amount of fish that can be caught, ban cigarettes, allow deforestation if it creates temporary jobs, etc.

In Economics, there are 4 types of resource (called the 'Factors of Production') that are used to make goods and services that people need or want. These are:

Natural resources - 'Land', trees in a native forest, rivers, iron ore/oil/rock/sand

People resources - 'Labour', teachers, lawyers, politicians, programmers, artists

Human-made resources - 'Capital', buildings, roads, trucks, ferries, computers

Enterprise - People who have an idea and bring the other three types of resource togetherHere's a short video clip that explains the 4 types of resource (Factors of Production), Opportunity Cost and Micro- and Macro-economics.

JUST watch to the 1:20 minutes point!

Activity 1

Imagine that there's a natural resource deep underground that can be used in power stations to generate electricity. Imagine that it burns cleaner than coal. Should we try to extract it? Maybe!

Now imagine that Entrepreneurs had an idea for a process, called 'Fracking', to extract such a resource. It uses capital resources (machines, pumps, chemicals, concrete), natural resources (water) and human resources (low wage workers). Should we use this process and the resources that it needs? Maybe!Well, the resource and the process of Fracking do exist. The resource is called Shale oil and gas. NZ and many countries allow companies to use 'fracking' to extract this natural resource. Others have banned the process.

Large profits can be made because the revenue from selling it is higher than the costs of drilling and transporting it. There are other costs, but drilling companies do not have to pay these - local residents pay these other costs!

Extracting Shale oil by Fracking uses resources that could be used by other entrepreneurs to produce different, less damaging products (eg wind and wave turbines). The benefits of the alternative products that we now can't have, because the resources are tied up in fracking, are called an Opportunity Cost of Fracking.

The Fracking process and disposing of its toxic waste, destroys other natural resources like clean drinking water, farm land for growing food and destroys the health and ability to work of human resources (local residents). These are large costs that the companies cause, but don't have to pay for and are called externalities.

Should we frack for shale oil and gas in NZ? Not so sure!? Watch these two videos and decide.

Accounting Cost is the money amount that we must pay (explicit cost).

In Economics, we also talk about Opportunity cost.

Opportunity Cost is the benefits that we miss out on because we've used our resources to produce one product and not another. For example, if you have $20 and pay for a movie ticket (and the enjoyment this gives you), you cannot have the next best alternative (perhaps the fun with your friends of buying a new basketball).

Economic Cost is Accounting Cost plus Opportunity Cost. For example:

If I buy wheat seeds and sow, water, fertilise and finally harvest them, I might have to pay $40 for seeds, water, my time, etc. I might sell the wheat for $100. My Accounting profit is $100 - $40 = $60

If I could have earned $55 from allowing campers to stay on the land, the Opportunity Cost is $55 (the next best alternative use).

My Economic profit from the wheat is $100 - $40 - $55 = $5. Because Economic Profit is a positive amount, I made a good choice to use my land, labour, capital & enterprise to grow wheat. I would have made $5 less profit from the next best alternative use of my resources.

Types of Economics

There are two types of economics:

Micro-economics studies individual industries and businesses eg competition, Monopoly power, Supply & Demand

Macro-economics studies whole country topics like inflation, growth, unemployment, investment, exports and trade.Real life example of Economics in action

The Ruataniwha dam in Hawkes Bay will flood a large area of land in order to provide irrigation water for increased dairy farming in an area prone to drought. Environmentalists say that it will damage the quality of water in the region, encourages a form of farming that is unsustainable in this dry area, and will use millions of dollars that could be better spent elsewhere.

Some investors want the scheme because they think it will generate large profits for them. However, the latest assessments estimate that farmers will not afford the high price the water will have to be sold at to cover the huge costs. This case study can be explained in terms of scarce resources, factors of production, opportunity cost, who gets to choose what is produced with our resources, micro- and macro-economics.

Here are two links to articles about the proposed scheme

2018 article: https://www.radionz.co.nz/news/national/360937/ruataniwha-dam-scheme-revival-raises-doubts-in-hawke-s-bay

2019 article: https://www.stuff.co.nz/environment/110889921/the-ruataniwha-dam-proposal-might-be-dead-but-now-another-dam-is-touted-on-the-same-river-with-ratepayer-funding-soughtActivity

Work in small groups to individually complete the Google Doc titled "Ruataniwha Dam" from Google Classroom. You'll need to read the article above and discuss who is affected, how the decision should be made and whether you think the scheme should go ahead.

- Understand how economic decisions impact on people, communities, and nations.

-

Learning Intentions

- To understand how limited resources affect what NZ can produce (and earn)

- Able to show in a graph how limited resources affect what can be produced in NZ

Production Possibility Curves (PPC)

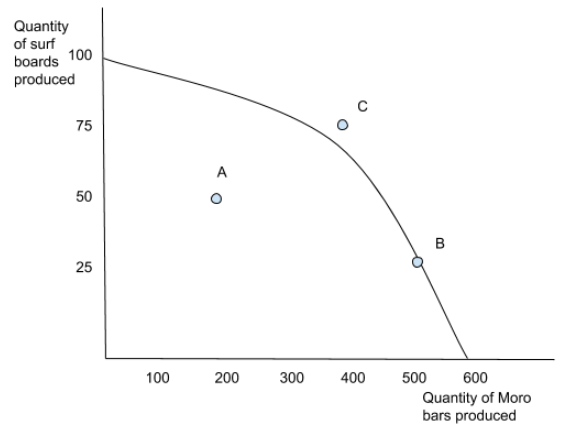

It is useful to show on a graph the maximum that we can produce with available scarce resources. To do this though, we have to pretend that we can only produce 2 products. Such a graph is called a PPC. Imagine that we can choose to produce surf boards and / or Moro bars. The curve below shows that we could produce any combination of these 2 products up to the line (eg points A and B, but not outside it (point C).

For example, we could produce 50 surf boards and 200 Moro bars (point A), or 25 surf boards and 500 Moro bars (point B). We do not have enough resources to produce 75 surf boards AND 400 Moro bars (point C).

Activity

Discuss in your group what would happen to the PPC curve (quantity that can be produced) if:

- more immigrants came to the country

- an earthquake destroyed factories and roads

- there were widespread floods across the country

- more efficient machines were developed that could produce more Moro bars

Activity

Watch this video clip of the NZ earthquake. Seeing the damage caused, think about what the effect was on the region's resources (land, labour and capital), ability to produce products and Production Possibility Curve.

Activity

Complete the Google Doc in Google Classroom called Intro to Economics. -

Learning Intentions

- To explore how supply and demand affect prices in a market

- Able to describe what causes changes in quantity supplied and demanded (and in supply & demand).

- Able to describe consequent changes in price, surpluses and deficits.

Supply curve

A supply curve plots price of a product against the quantity supplied (by producers).

It slopes from bottom left to top right, because the higher the price, the more producers want to make and sell it.

We assume that only one 'variable' changes at a time.

If price of the product increases, we move to a new point along the curve - called an increase in quantity supplied.

If price stays fixed, but one other 'variable' changes (eg productivity, cost of raw materials), then the curve itself shifts to the right (increase in Supply) or to the left (decrease in Supply).Demand curve

A demand curve plots price of a product against the quantity demanded (by consumers).

It slopes from top left to bottom right, because the higher the price, the fewer consumers want to buy it.

We assume that only one 'variable' changes at a time.

If price of the product increases, we move to a new point along the curve - called a decrease in quantity demanded.

If price stays fixed, but one other 'variable' changes (eg incomes, prices of other related products), then the curve itself shifts to the right (increase in Demand) or to the left (decrease in Demand).Activity

Complete the Google Doc in Google Classroom called Supply / Demand Activities. -

Learning Intentions

- To explore the ways people earn income.

- To explore the 'Labour Market' and the relative gains of wealth and income.

- Can describe different types of income and tax.

Income

The Labour market is the way in which suppliers of labour (workers) and those that demand (and pay for) labour (businesses) come together to exchange.

Consider whether the labour market is fair! Discuss whether Neymar is worth $90 million per year, (Ronaldo $108M and Messi $111M). Explain why you think this. Then discuss whether nurses or less valuable to society than football or basketball players? Discuss whether the pay you receive reflects the value society places on you, or whether it reflects some other factor.

Answer the questions in the activity on Google Classroom called "Income".

Types of income

Wages are based on an hourly rate multiplied by the number of hours worked. They are often paid for manual work, eg in the building and retail industries.

Salaries are stated on a yearly basis, although they are paid in instalments, normally every two weeks. The same amount is paid, no matter how many hours are worked! Teachers, managers, accountants are usually paid this way.

Independent contracting is when a person with specific skills works for a business to do a specific task, normally for a set period of time and for a set amount of money. At the end of the contract, they find a new contract for a new client. Contractors are viewed as self-employed.

Sales commission is a percentage of the value of the product that is paid to the sales person or agent. This is how Real Estate Agents are paid. This provides an incentive to sell lots. Sometimes, you might receive a set wage or salary, with commission paid on top.

Royalties are similar to commission, but are paid to an author or artist when their text, music, artwork is used.

Interest is received when you have savings in a bank or other financial institution. This is a form of income. If you win the lottery and save the money in a bank, you might be able to take out the interest each month and live on this - just!

-

Learning Intentions

- To explore how financial information is used to make decisions.

- To explore good practice in spending, saving and borrowing and with a professional.

- Can describe different types of income and tax

- Can describe the ways that taxes are used by the Government.

Introduction to tax

The Government needs to raise funds to pay for public services (eg healthcare, police, nurses, schools) and infrastructure (eg roads, national parks). The main way in which they raise these funds is through taxes. In NZ, just under $100 billion is collected each year.

The main types of tax are:

1. Income Tax (PAYE)

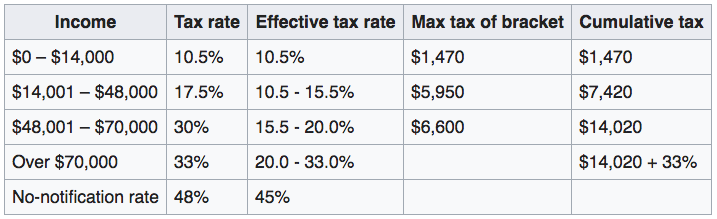

Pay As You Earn (PAYE) is deducted from wages and salaries, before you receive the money. It is a 'Progressive Tax', meaning that if you earn higher income, you pay a higher percentage of your income in tax. We'll discuss the table below, but in simple terms it shows that:

- if you earn $14,000 you pay 10.5% ($1,470). I

- if you earn $14,100 you pay 10.5% on the first $14,000 and 17.5% on the extra $100; that's tax of $1,470 plus $17.50 which totals $1,487.50.

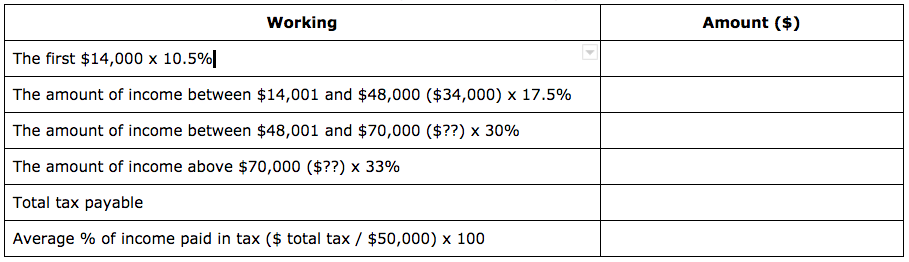

Activity: Calculate the income tax that you would pay if you earned $50,000 pa. The table below will help you.

2. Goods & Services Tax (GST)

Most goods and services that are purchased incur GST at 15%, which is added on to the basic cost of the products (eg if you buy a shirt for $115 in the shop, $100 is for the shirt and $15 is tax that the shop keeper passes on to the Government).

3. Company Tax

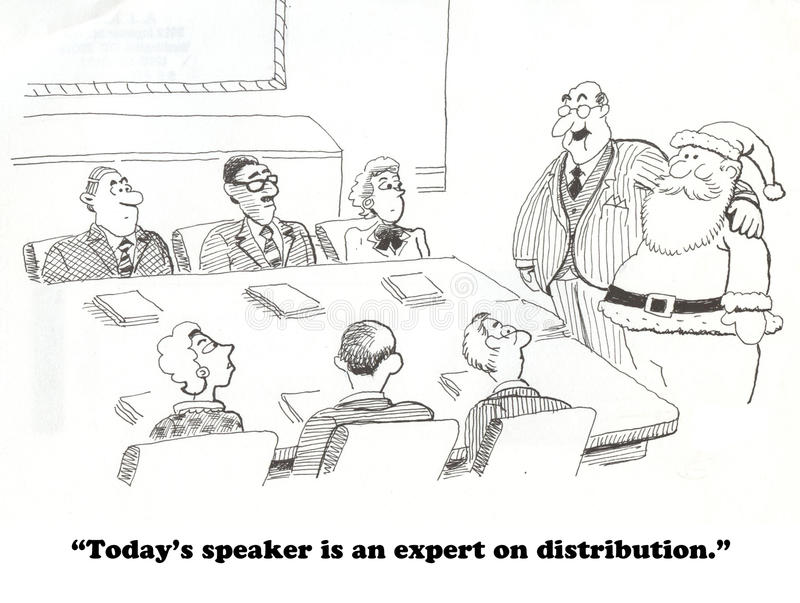

Companies pay 28% of net profits as tax. This is a flat rate - large and small profits are all taxed at the same 28%.Activity

1. In small groups, try to explain the 'multinational' cartoon above. Multinationals are companies that operate in several countries.

2. Discuss what might be disadvantages of large multinationals operating in NZ.

3. Discuss any benefits that companies like Google and Facebook bring to NZ

Here are some interesting resources on this topic:

- https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11607336

- https://www.beehive.govt.nz/release/multinationals-tax-legislation-introduced

- https://www.rnz.co.nz/news/political/496826/government-unveils-digital-services-tax-aimed-at-multinationalsIRD numbers and deductions

The Inland Revenue Department issues you a IRD number when you start work - if you ask for one. It's important because they charge a very high 'default' tax rate if you do not have a number. You also need a IRD number if you earn interest or have a KiwiSaver account.

Deductions are made from your income for a range of things. Some are included in the PAYE income tax calculation (eg Accident Compensation or ACC, and student loan repayments). ACC is similar to insurance and pays for health care following accidents that New Zealanders have. Student loans do not have to be repaid until you start working. Your repayments are 12% of any income over $19,136 pa. Other deductions are pension contributions, like KiwiSaver. -

Learning Intentions

- To explore business aims and objectives, and the conflicting interests of different stakeholders.

- To explore how business impacts on society and how pressure groups and government can influence decisions.

- To explore why some businesses are run sustainably and 'environmentally', and some are not.

- Can explain different business goals that influence an issue.

- Have raised awareness or advocated a change of practice, beyond school (eg article presentation, emails)

- Can describe different stakeholders in a business issue.

You should by now have looked through the resources on business issues (eg pollution, health) and chosen an issue that is of interest to you.

Research the winners and losers in this issue and the organisations that should protect the 'losers' and that are enabling the 'winners' to continue.

Try to understand exactly why the problem continues and what the costs are on all the people involved.

-

Now you have a full understanding of your business issue - it's causes, effects, enablers (those allowing it to continue) and potential change agents (those that could change it), it's time to finish drafting your poster, slide presentation, email list, news article, etc. In other words, it's time to DO something to change things.